Could “Temporary Deflation” follow the “Temporary Oil-Driven Spike in Inflation”?

*The dramatic spike in oil prices generated 3 months of outsized increases in CPI and PCE inflation that pushed up their yr/yr measures.

*The Fed has kept rates on hold and did not accommodate the negative supply shock, core inflation measures have not increased much, and inflationary expectations have remained anchored.

*Oil prices have fallen sharply, and if current prices stick close to current levels (around or below $75/barrel)—which is uncertain as inventories need rebuilding–continued rapid price declines in gasoline and other energy may result in several months of declines in the CPI and PCE Price Index.

*This would ease some price pressures on consumers and let the Fed breath more easily.

In a note in mid-April, I described how the spike in oil prices from $65/barrel to $95/bbl would temporarily boost the monthly inflation data for about three months as retail prices adjusted to the higher oil prices. I emphasized the importance of the Fed not accommodating the negative supply shock, which would keep its impacts temporary, limit the pass through of the higher oil prices to the prices of nonenergy goods and services, and constrain inflationary expectations. I noted that if oil prices remained around $95/bbl, after several months of outsized increases, the monthly inflation data would revert to their prior increases, while their yr/yr measures would rise to absorb the temporary monthly spikes.

I continued: “However, if oil prices fall, subsequent months’ CPI and PCE Price Index data would possibly decline, and the temporary months of deflation would reduce the general price level from its oil price-driven peak.” That process is now beginning to unfold. Yippee: a positive supply shock that involves a partial reversal of the negative supply shock imposed by the conflict in the Middle East and relief to consumers and businesses.

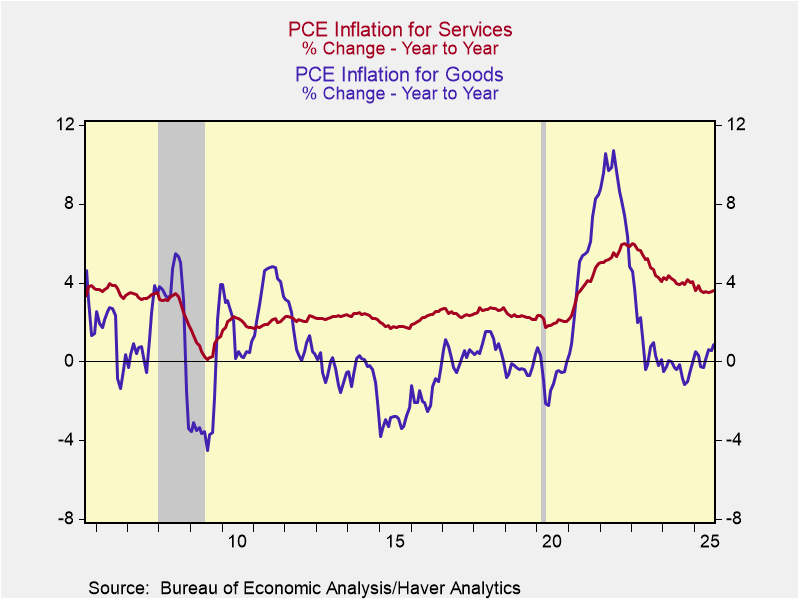

Here’s the situation: in the prior 12 months through February 2026, CPI inflation was 2.4%, averaging a 0.2% increase per month, while PCE inflation was 2.9%, averaging a 0.3% rise per month. The oil price spike pushed up CPI inflation 0.9%, 0.6% and 0.5% in March, April and May, lifting its yr/yr inflation to 4.2% in May, while PCE inflation rose 0.7% and 0.4% in March and April, lifting its inflation to 3.8% in April (PCE inflation for May will be reported tomorrow). See Chart 1. During these months, both core CPI inflation and PCE inflation rose a bit (CPI: 0.2%, 0.4% and 0.2%; PCE: 0.3% and 0.2%), but the details of the CPI indicate that the pass through of the oil price spike was fairly limited to specific categories, including energy services (electricity and utilities) and airline fares. Most categories in the CPI showed little effect of the higher oil prices.

Chart 1. CPI Inflation and WTI Oil Prices

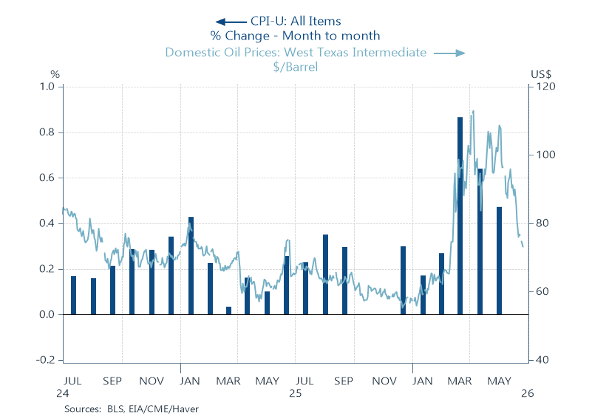

The fall in oil prices will start to show up in the June inflation data and be much more pronounced in the July data. Declines in monthly CPIs are fairly rare, but do occur, particularly when large declines in oil prices generate falling gas and energy prices, like in late 2014).

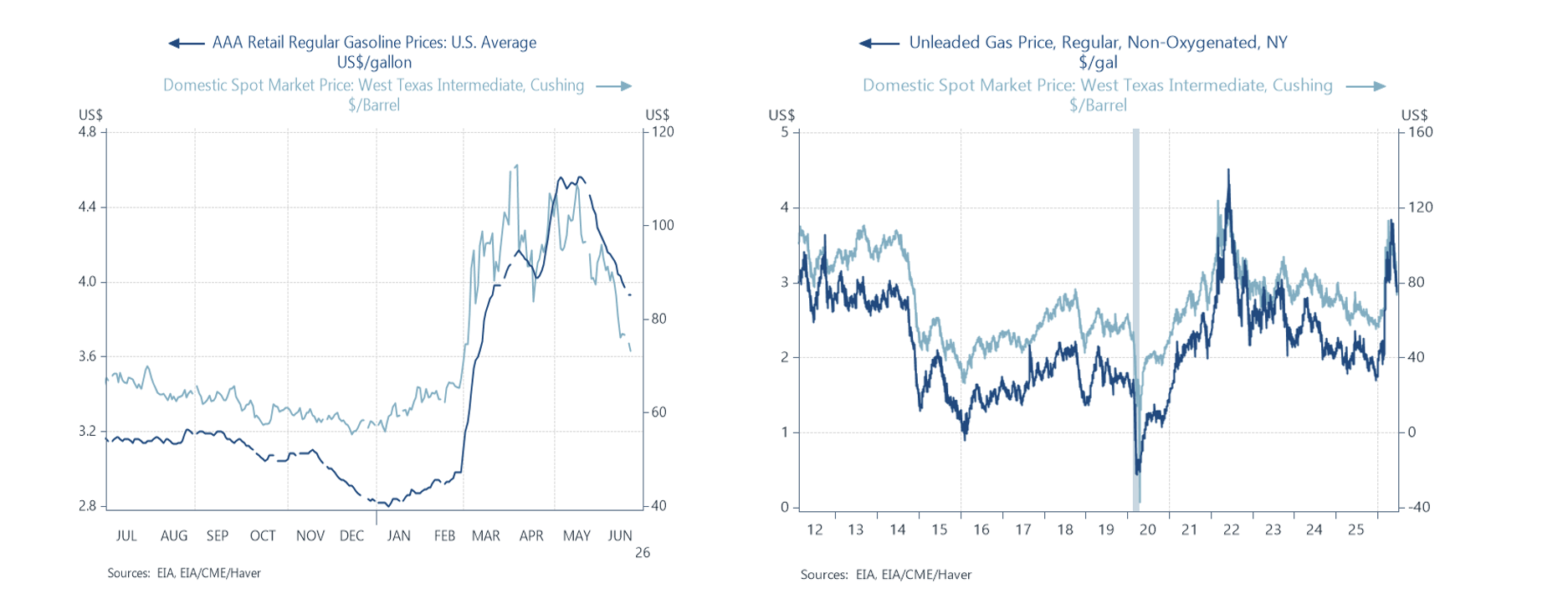

WTI oil prices averaged $97.8/bbl in May and have fallen sharply, averaging $75/barrel in the last week. At this writing, they are around $72/bbl. The speed of the decline in crude oil prices has been impressive, and contrary to the warnings by oil experts that the rebuilding of global oil inventories would keep oil prices high. Thanks to the ramping up of domestically-produced oil, refined products are plentiful. So far, retail gasoline prices have also fallen rapidly, consistent with their historical pattern of adjusting quickly to changes in crude oil prices (Chart 2).

Charts 2. WTI Oil Prices and Retail Gas Prices

In the first three weeks of June, when oil prices have averaged approximately $86.5/bbl, gasoline prices averaged $4.16/gallon, down from their $4.50/gallon average in May. These declines in retail gas prices should be reflected in the June inflation data, enough to ease the monthly increase in the CPI and PCE Price Index. The CPI should also get some relief from lower prices of airfares, where anecdotal evidence suggests some easing of prices. On the other hand, energy-related surcharges on distribution costs and other services are expected to be slower to adjust to the lower gasoline and energy prices.

If oil prices hold anywhere close to current levels, outright declines in the monthly inflation measures would be likely. They would reduce the yr/yr inflation back toward its pre-oil price spike levels. That would make the March-May oil price shock truly temporary.

A note on the term “temporary”. The Fed’s reference to the surge in inflation beginning in 2021 as a “transitory supply shock” was erroneous and misguided. While the Covid pandemic bottled up global supply chains and was a temporary negative shock to supply, the unprecedented fiscal and monetary stimulus (deficit spending was increased by 25% of GDP and the Fed reduced rates to zero and effectively purchased one-half of the increase in Treasury bond issuance) generated the strongest acceleration of aggregate demand in modern U.S. history, which obviously contributed to the high inflation. The Fed, which had presumed inflation would stay low as it did during the recovery from the Great Financial Crisis, called the rise in inflation “transitory”, and subsequently, it purposely chose to understate (ignore) its role in generating the surge in inflation, instead blaming it on a negative supply shock. Also, remember that after the surge in inflation, the Fed emphasized that its goal was to reduce inflation to 2%, thus accepting the permanently higher general price level that it had contributed to.

In response to the recent oil price shock, if the Fed had accommodated it, the temporarily higher monthly inflation could have become a more permanent one. But the Fed wisely kept monetary policy on hold, so its inflationary impact will be temporary. Now, the lower oil prices hold the prospect that the general price level will fall and partially reverse some of its sharp rise during the negative supply shock.

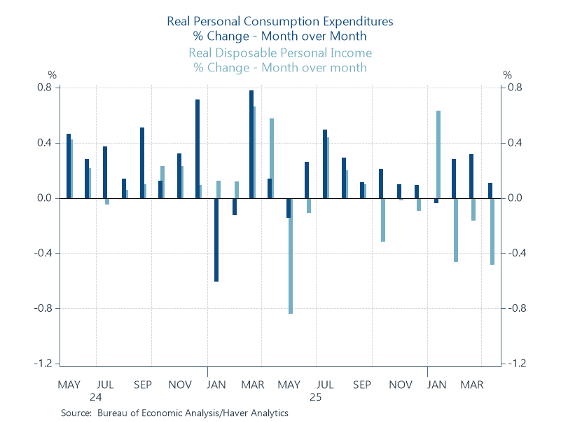

Consumer spending patterns. Consumers have remained resilient. While the three months of spikes in inflation have resulted in declines in real disposable personal income, inflation-adjusted consumption has continued to rise (Chart 3). On average, consumers have drawn down their rate of personal saving of disposable income and smoothed spending (in April, the rate of personal saving fell to 2.6%, close to an all-time low). The continued rise in consumption has been aided by several factors: following a period of weakness, employment payrolls have increased in each of the last three months; last year’s tax cut package increased tax rebates in Spring 2026; and rising household net worth has supported higher propensity to spend. Of note, in contrast to prior surges in oil and gas prices, motor vehicle sales rose a bit during the three months March-April-May when gasoline prices surged.

An easing of inflation–or better yet a reversal of the recent inflation spikes with some temporary (couple of months) of deflation–would provide relief for consumers and increase their purchasing power. That relief would come during peak seasons for driving and electrical services usage

Chart 3. Real Consumption and Disposable Income

The Fed’s monetary policy. The Fed is to be commended for not accommodating the negative oil supply shock. At its June FOMC meeting and at Kevin Warsh’s first post-FOMC meeting press conference, Warsh made clear that reducing inflation to the Fed’s 2% target was a priority, and he moved away from the Fed’s earlier characterization that monetary policy was mildly restrictive. In its updated June Summary of Economic Projections, the FOMC members estimated that a rate hike may be appropriate to be consistent with its dual mandate. But the FOMC member dots are not binding, and subject to changing conditions.

Could a bout of temporary deflation change the monetary policy landscape? Yes. Of course, the Fed’s monetary policy deliberations would depend on core inflation, but several months of deflation would raise the real Fed funds rate and change the environment. Warsh and the Fed favor lower inflation, but Warsh is also practical. I doubt if the Fed would vote to raise rates in an environment in which the general price level is declining.

Stay tuned.

Are Current Credit Conditions Worrisome?

In an interview earlier this week, Jamie Dimon, CEO of JPMorgan, said "banking rivals are doing dumb things" and drew parallels between current credit conditions and those in the years leading up to the 2008-2009 Great Financial Crisis. Immediately following Dimon's interview, the FDIC issued its "Quarterly Banking Profile,” which provided evidence that commercial banks are in sound shape financially, with relatively high levels of capital and fairly low loan delinquencies. Private credit has also been in the news, fueling fears of real problems. Private credit is not supervised and there are no reliable sources of data for evaluating private credit. This makes financial markets vulnerable to speculation and anecdotal evidence.

Are current credit conditions worrisome? My current assessment is that as long as the economy continues to expand, with aggregate demand growing anywhere near its recent pace, commercial bank credit is not worrisome, and credit conditions are far different than the problems and risks that characterized the pre-GFC period. If the economy were to fall into recession, resulting in a decline in business revenues and profits, credit problems would obviously emerge, but current monetary and fiscal policies suggest the probability of that outcome is low.

The rapid growth of private credit may be a problem. However, if problems exist, most likely they are largely concentrated in the debt-financed AI infrastructure buildout, and a deterioration in private credit conditions would have localized economic and financial impacts, unlike the GFC. Unfortunately, there is insufficient collected information and data to assess the situation, so understanding the scope of the credit issue must be based on specific credits, cash flows and capital of companies.

Dimon's concerns about parallels to the pre-GFC credit markets seem overstated. Consumer and business debt and debt-service are in fairly good shape and current credit conditions and banking practices are far different than during the pre-GFC. Corporate America has been deleveraging for years, household debt remains relative low compared to disposable personal income, and commercial banks are largely well capitalized and have a better understanding of the risks in their balance sheets.

In the years leading up to the GFC, nearly the opposite unfolded. There was an explosion of mortgage debt during an unruly bubble in housing activity (national outstanding mortgages rose 75% in the years 2002-2008) driven by rapidly rising home values and excessively loose credit standards (mortgages, HELOCs, home equity loans); a proliferation of overly-complex MBS and ABS derivatives that created tranches of income-yielding securities that were widely held by banks and investors who didn't know their risks; and insufficient bank capital and lax definitions of capital held by banks. Expectations that home values would continue to rise forever were the catalyst that drove the housing and mortgage demand and loose bank credit standards and willingness to hold complex and risky MBS derivatives. There was a high degree of interconnectedness of systematically important financial institutions (SIFIs) that risked contagion.

When home prices and expectations of future values began to fall in Spring 2006, the entire mortgage market began to unravel. Collapsing values of MBS derivatives and massive mortgage defaults resulted in back-breaking losses for banks, revealing insufficient bank capital bases. Widespread uncertainties about banks' capital led to a short-term funding crisis for large banks, a dramatic spike in uncertainty and broader financial paralysis and deep economic contraction. In sum, real estate loans were at the heart of commercial banking portfolios, and the credit quality of the loans were rotten.

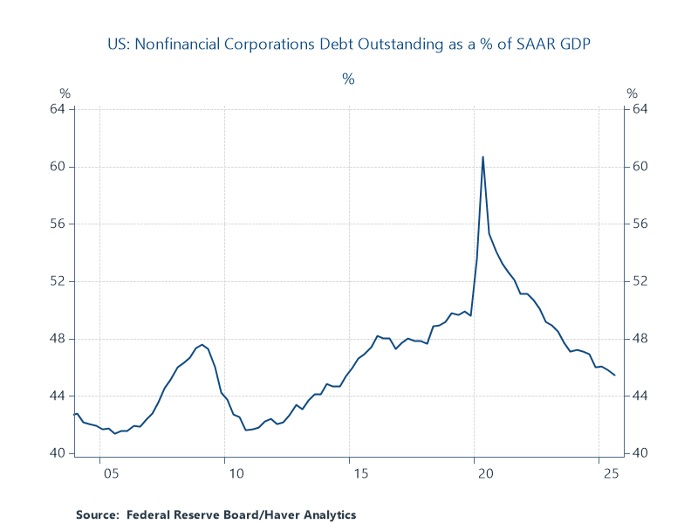

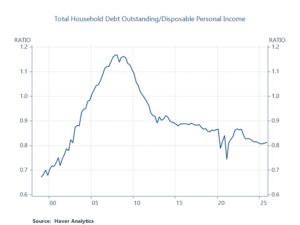

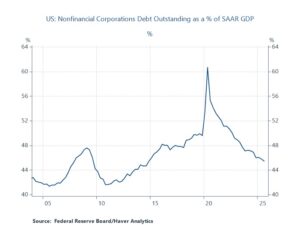

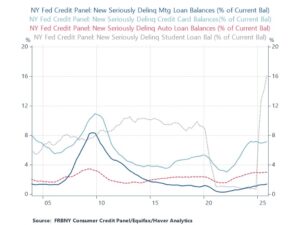

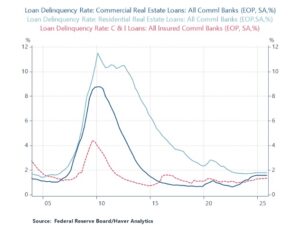

The most recent Federal Reserve reports on commercial bank balance sheets and household debt along with the FDIC Report show that household and business debt levels are not high relative to economic activity and disposable personal income, and banks remain healthy and well-positioned. Chart 1 shows total household debt including mortgages as relatively low as a share of disposable income while Chart 2 shows that business debt is falling as a share of GDP. Chart 3 shows the shares of consumer loans by type: excluding the policy-induced spike in student loan delinquencies, the only concern is credit card debt where seriously-delinquencies are uncomfortably high. Chart 4 shows delinquencies of business loans: delinquencies of commercial real estate loans have risen only modestly since the Covid-related spike in commercial real estate vacancies in big cities and remain below delinquencies of residential real estate loans. Recent indicators suggest that the problems in commercial real estate are now diminishing.

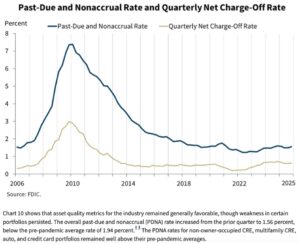

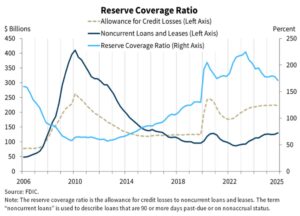

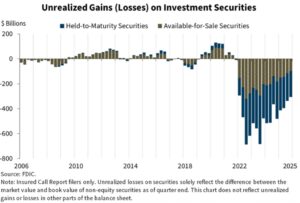

Charts 5-7 are from the recent FDIC Report: they show that banks' past-due loans and leases and charge-offs are relatively low; their reserve coverage ratio is relatively high; and their unrealized capital losses of investment securities is shrinking (banks have reduced the duration of their securities and longer-term yields have declined). The FDIC tabulation of problem banks is low. All-in-all, commercial banks are in relatively good shape.

The private credit market remains murky, except for those who are directly involved — the lenders and their sources of capital and leverage--and have access to the financials of the credits they are involved in. The lower costs and higher efficiencies of private lending that stems from lower costs of supervision and government regulatory oversight has a downside: lack of knowledge of data and transparency. In a recent study by the Alternative Credit Council and Houlihan Lukey, Financing the Economy 2025, the private credit market is described in broad terms and includes many interviews with active private creditors, but it does not include the sufficient data to analyze and evaluate private credit. (In a recent article I co-authored with Amit Seru, “The Fed Needs to Earn Its Independence. Just Setting Rates Isn’t Enough,” we argued that the Federal Reserve should seek to obtain information on the credit activities of the private lenders.)

It's important to distinguish between the different kinds and structures of private credit. Some (many?) private creditors are basically making the loans that commercial banks used to make, benefiting from the lower costs of supervision, compliance and regulation. They raise private capital, leverage it with loans from commercial banks, and provide credit to borrowers at healthy spreads. They conduct credit analyses of their clients. Presumably, the credit quality of their loans does not deviate significantly from the commercial and industrial (C&I) loans of commercial banks, although that is not ensured. Also, it is likely that most private creditors are less leveraged than banks.

Two of the largest concerns with private credit are 1) that the proliferation of private lending may be diluting the quality of the private creditors and lessening their credit standards and oversight of the loans, and 2) some private lenders have a narrow focus of their lending activities, and their lack of sufficient diversification may generate concentrations of defaults.

Currently, there's a ton of news on the rising debt used in the AI infrastructure buildout, including data centers and energy production facilities. Sorting out the corporate finances of the companies leading the AI capital spending buildout is difficult. For many companies involved in the AI buildout, much of the capital spending on data centers and energy related buildouts has been financed with internal capital and cash flows. More recently, however, a significant amount has been financed by debt. At the same time, the revenues and free cash flows generated by AI-related products are accelerating dramatically. Based on standard business metrics, a snapshot of the finances of many of the largest AI firms are reasonable or even good. Several may be problematic.

The pace of implementation of AI into commerce and society is stunning. Most likely it will add materially to productivity, economic growth and profits, and will disrupt labor markets. As with all other innovations in U.S. history, disruptions will result in some jobs lost and other new jobs created. I take a positive view of longer-run outcomes. In weighing current commentary on the labor market outcomes stemming from AI innovations, be careful in extrapolating anecdotal evidence to the entire economy, and remember the adage “bad news sells.”

As with all episodes of technological innovation in the U.S., there will be some failures among the AI innovators, and some of the providers of capital and credit will incur losses. However, in contrast to the GFC, the losses will be incurred by a narrow group of capital and credit providers and will not be pervasive and unhinge society and commercial banking. Consider an insurance company or a state pension that finances an AI project and incurs a sizable loan default or capital loss. The jarring impacts of the losses will be narrowly focused and would be relatively minor to the broader commercial banking industry. Similarly, the impacts of the large losses stemming from the Covid-initiated collapse of commercial real estate in big cities were relatively narrow and didn’t unhinge the banking industry. The private credit industry and AI require scrutiny. A close assessment of individual company products, revenues and profits and capital spending is required. This may be a time to be cautious in private lending. But starting with the premise that we should be fearful because it has parallels to the pre-GFC period is not particularly instructive.

Chart 1. Household Debt Outstanding/Disposable Personal Income

Chart 2. Non-financial Corporate Debt/GDP

Chart 3. Seriously Delinquent Consumer Loans and Mortgages

Chart 4. Delinquencies of Business Loans

Chart 5. Past-Due and Charge-Off Rate

Chart 6. Bank Reserve Coverage Ratio

Chart 7. Unrealized Losses on Bank Investment Securities

Keep an Eye on Real Wages and Hours Worked in Economy

U.S. economic growth has remained solid through most of 2025, driven by healthy gains in consumption and strong business fixed investment, particularly for the buildout of AI. This has defied the pessimists’ worries about President Trump’s misguided tariffs, clampdown on immigration and cuts in research grants to universities. The only real laggard in 2025 was the housing sector, which suffered from continuous declines in spending on construction and improvements. But that was last year and we should not expect any let up in erratic tariff policies and anti-immigrant initiatives in 2026.

Despite these obstacles, the outlook for sustained expansion in 2026 looks favorable, and the probability for recession is low. Current conditions are inconsistent with onsets of recession in the past. Consider the following two items that will support aggregate demand: 1) three Fed interest rate cuts in September-December 2025 lowered the real Fed funds rate below the Fed’s estimate of the longer-run real rate of interest consistent with its dual mandate of 2% inflation and maximum employment, and the Federal Reserve Bank of Chicago’s Financial Conditions Index signals loose financial conditions, and 2) fiscal policy is stimulative, as the OBBBA of 2025 extended the 2017 tax cuts and added some additional cuts (eliminating tax on income from tips, expensing of outlays for research and development) that will boost tax refunds in Spring 2026 by approximately 0.6% of disposable personal income. In this environment, 3) business inventories are relatively low and 4) employment is well-aligned with output (GDP). Accordingly, any slump in aggregate demand will not force businesses to cut output and/or employment in a meaningful way.

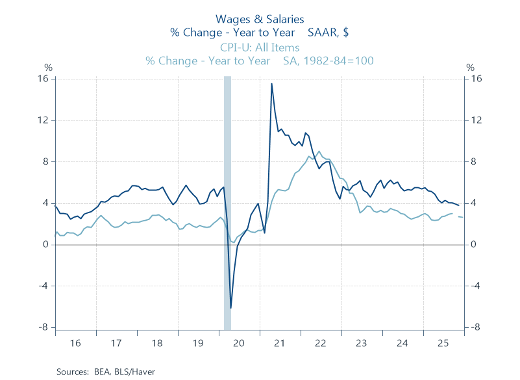

Labor market and personal income dynamics. One key trend to keep an eye on is real wage and salary incomes, a key indicator of labor market conditions and measure of consumer purchasing power. Growth in personal income from wages and salaries has decelerated to 3.8% in the year ending November 2025 (Chart 1). That’s down from a 5.5% rise in the prior year. At the same time, CPI inflation was 2.7% in the last two years ending November 2025. According, the year-over-year growth in real personal disposable income from wage and salaries has receded to 1.1% in the year ending November 2025, significantly slower than its 2.8% rise in the prior year.

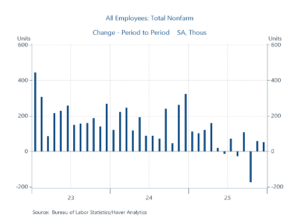

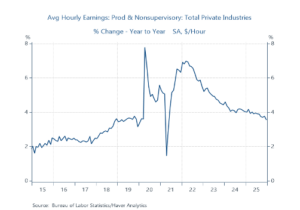

This deceleration in real wages and salaries reflects primarily a combination of moderating gains in average hourly earnings (AHE) and weakness in employment. As shown in Chart 2, AHE have moderated to 3.5% year-over-year growth from 4.1% a year earlier. The yr/yr rise in AHE will decline further in the January and February 2026 readings as the high monthly increases in Jan-Feb 2025 roll off. At the same time, establishment payroll gains have flattened significantly. In the six months July-December 2025, employment rose a net 87,000, an average of 14k per month; in the prior six months jobs rose 497k, an average monthly rise of 82k (Chart 3). In the prior year ending December 2024, employment rose over 2 million.

Chart 1. Wages and Salaries and CPI Inflation

Chart 2. Average Hourly Earnings

Chart 3. Establishment Payrolls

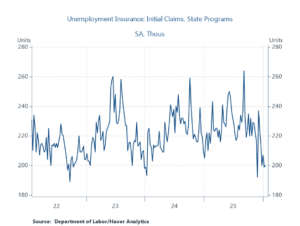

The flatter employment gains and weakening of labor markets is a product of less supply of labor and weaker demand. Trump’s clampdown on immigration has clearly constrained the supply of labor. It has probably also dampened business demand for labor, particularly in construction and leisure and hospitality sectors. Businesses have responded by slowing hiring while the high costs of search and hiring have reduced their layoffs. Initial unemployment claims have remained low (Chart 4).

Chart 4. Initial Unemployment Claims

Amid slower gains in employment and average hourly earnings, the positive in labor markets is aggregate hours worked increased 0.7% in 2025. That’s fortunate insofar as wages and salaries and disposable personal income are driven by hours worked, not employment. Importantly, stronger productivity gains have powered the solid economic growth. During the year ending 2025Q3, productivity (private output/aggregate hours worked) in the nonfarm business sector rose 1.9% and 2.3% in the manufacturing sectors. This decided pickup in productivity reflects the continued momentum in business investment in data storage and related AI infrastructure plus production efficiencies stemming from broadening uses of AI innovations in both manufacturing and service-producing industries.

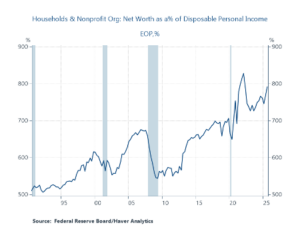

The wealth effect and rate of personal saving. Most households spend most of what they earn, so consumption will be driven largely by growth in disposable income. In addition, the ongoing surge in household net worth, reflecting the rise in equity valuations and real estate, has lifted the propensity to spend. In the last year, household net worth has risen 7.6% to an all-time high of $181 trillion. To put it into perspective, household net worth has risen to 7.9 times the annual flow of disposable personal income (Chart 5). The sharp increases in household net worth are adding to the flow of disposable income (through required minimum withdrawals of IRAs and private pensions and gifting and the like) and boosting consumption through the positive wealth effect--increasing the propensity to spend out of disposable income. As a result of the sizable wealth effect, the rate of personal saving declined to 3.5% at its last reading in November 2025. It cannot be expected to fall much further.

Chart 5. Household Net Worth/Disposable Personal Income

Add it all up, and consumer purchasing power, driven by employment, hours worked and average hourly earnings, are key variables to follow in 2026. The highest probability outlook is continued expansion at a slower pace of growth.

Mickey D. Levy is a Visiting Fellow at the Hoover Institution at Stanford University and a longstanding member of the Shadow Open Market Committee

Monetary Policy Responses to Shocks

Here's a paper and presentation that I co-authored with Dr. Michael Bordo and presented at the November 2025 Shadow Open Market Committee meeting. "Monetary Policy Responses to Shocks" analyzes the history of shocks — the Great Inflation of 1965-1982, the Great Financial Crisis and Covid, plus an array of minor disturbances — and how the Fed responds to them. We find that the Fed has responded unsystematically, and often in ways that extend and accentuate the costs imposed by the original shock.

Paper: Monetary Policy Responses to Shocks (Michael D. Bordo and Mickey D. Levy, Nov. 7, 2025, Shadow Open Market Committee)

Power Point: Monetary Policy Responses to Shocks (Michael D. Bordo and Mickey D. Levy, Nov. 7, 2025, Shadow Open Market Committee)

The SOMC meeting, the first in its partnership with the Center for Financial Stability, included great presentations on Fed independence, Fannie and Freddie, and financial stresses.