Economic Policy and Financial Insights

Is the U.S. Economy Fragile or Resilient? And a Note on Aggregate Demand and Inflation

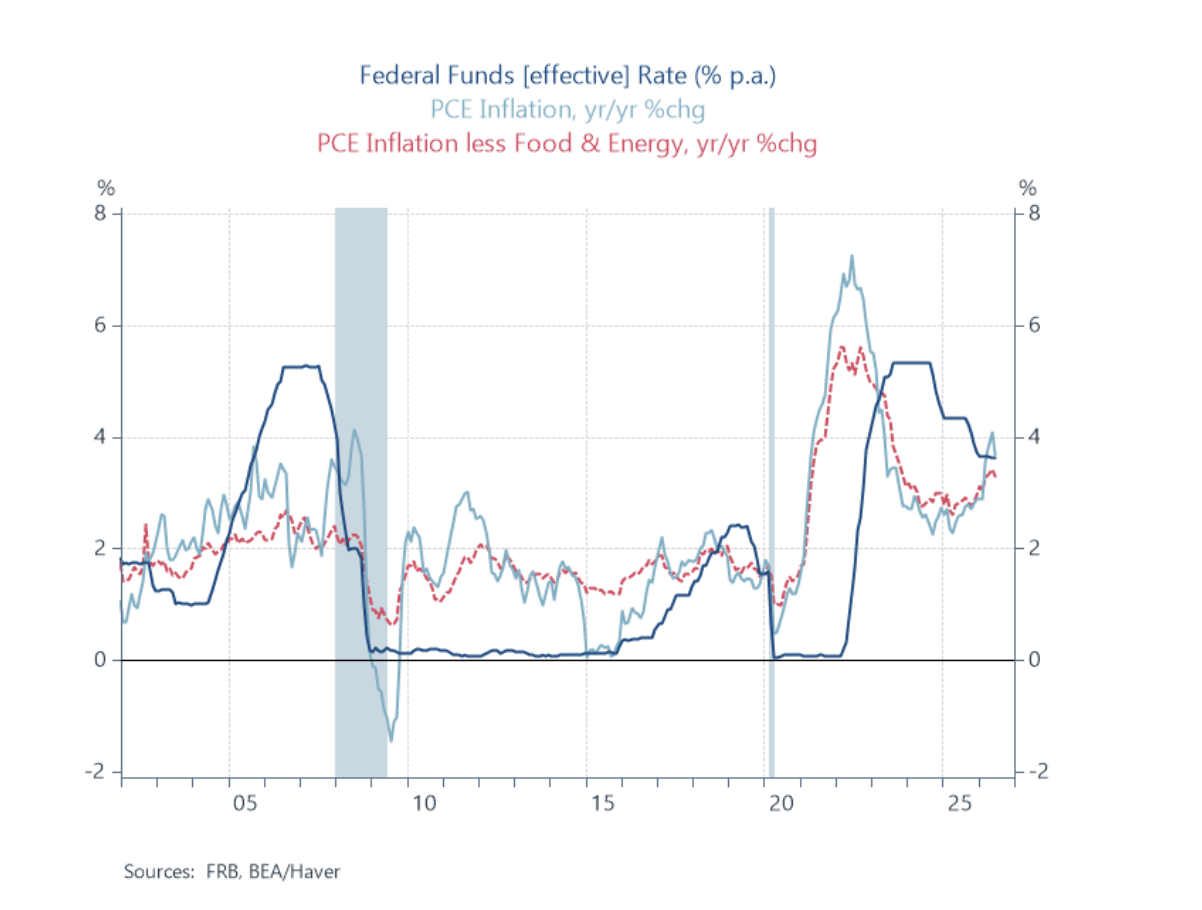

In this paper, I describe how the U.S. economy has been resilient in response to shocks, and that the undesired inflation has been generated by rapid growth in aggregate demand that must be slowed to reduce inflation to desired levels.

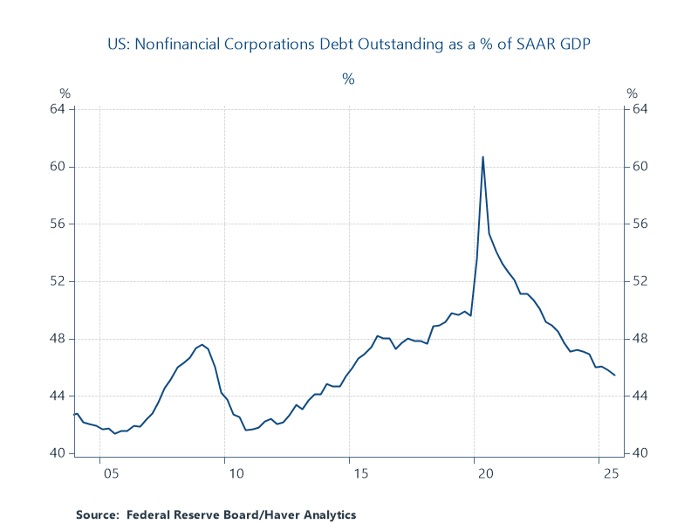

Are Current Credit Conditions Worrisome?

Are current credit conditions worrisome? In this paper, I assess credit conditions in the banking and private credit market, with a particular focus on debt related to AI. I find that commercial banking conditions are sound and while private credit may be problematic, if credit problems do emerge they will be narrowly focused and do not pose a threat to financial stability. Drawing parallels between current credit conditions and those leading up to the Great Financial Crisis, as JPMorgan's Jamie Dimon did last week, is inappropriate.

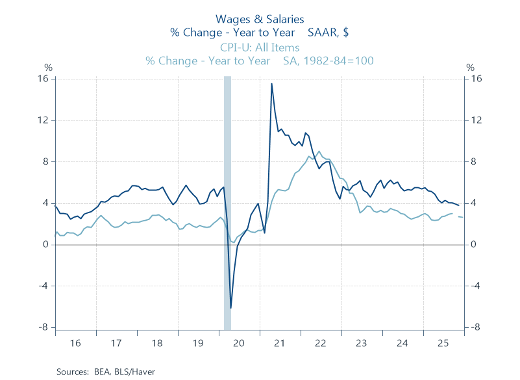

Keep an Eye on Real Wages and Hours Worked in Economy

Following the solid gains in U.S. consumption in 2025, this essay dissects the key factors driving disposable personal income — employment and hours worked, average hourly earnings and income from wages and salaries — and concludes that the growth in consumer spending will continue to grow, but weaker fundamentals point to a moderate pace in 2026.

Monetary Policy Responses to Shocks

Here's a paper and presentation that I co-authored with Dr. Michael Bordo and presented at the November 2025 Shadow Open Market Committee meeting. "Monetary Policy Responses to Shocks" analyzes the history of shocks — the Great Inflation of 1965-1982, the Great Financial Crisis and Covid, plus an array of minor disturbances — and how the Fed responds to them. We find that the Fed has responded unsystematically, and often in ways that extend and accentuate the costs imposed by the original shock. The SOMC meeting, the first in its partnership with the Center for Financial Stability, included great presentations on Fed independence, Fannie and Freddie, and financial stresses.

Reflections on Jay Powell’s Jackson Hole Speech

Here's an assessment of Fed Chair Jay Powell's speech at the annual Jackson Hole symposium that focuses on how the Fed revised its misguided 2020 Strategic Plan back to its original, balanced Consensus Statement of 2012, and pays tribute to my colleague Charlie Plosser, former President of the Federal Reserve Bank of Philadelphia and a key architect of that 2012 Plan and the Fed's 2% inflation target, who passed away last week.

Macro Minds With Kallum Pickering

Here's an interview on the Podcast "Macro Minds," hosted by Kallum Pickering, Chief Economist of PeelHunt, a leading UK investment bank. We discuss the impact of tariffs from a global perspective, and related topics like how the tariffs will impact global trade and how countries have varying degrees of flexibility to negotiate with President Trump. We also review current economic conditions in the U.S., how the Fed may respond and the implications for financial markets, and in light of Trump's erratic behavior, we consider how different scenarios may unfold.

An Opportunity to Improve the Fed’s Strategic Framework

Yesterday, the Shadow Open Market Committee's meeting in Washington, D.C. addressed issues of how the Fed may improve its policy framework. Here are a paper and presentation I prepared on the issues with Charles Plosser, former President of the Federal Reserve Bank of Philadelphia. We describe how the asymmetries of the 2020 strategic plan, particularly its FAIT scheme and dropping of preemptive monetary tightening, was driven by the Fed's excessive fears of too-low inflation and the Effective Lower Bound. We recommend restoring symmetry to the strategic framework, in part by re-establishing a clear symmetrical 2% inflation target, and encourage the Fed to consider systematic rules as an input to its discretionary conduct of monetary policy. We recommend many changes to the quarterly SEPs: its infamous dot plot should include a Taylor Rule estimate (dot) of the appropriate interest rate that would achieve the median FOMC economic and inflation projections; information about the Fed's balance sheet; and an annual scenario analysis exercise with alternative projections. In contrast, I'm sure the Fed's currently ongoing strategic review will be a tame and closely controlled review.

China’s Stimulus Boosts Markets, but Expected Economic Impact Modest

In reports in recent years, I have described the transition of China’s economic structure and its government-generated excesses in real estate, and warned that its adjustments would dampen its economy for years to come. Everything is unfolding as predicted.

A Comparison of the Biden and Trump Economic Platforms

This paper provides a comparison of the economic platforms of Biden and Trump. I purposely do not analyze the economic effects of the platforms or their specific provisions and try to be even-handed in my descriptions (and stay clear of personality and leadership issues). The implications for economic performance, in the U.S. and globally, are important. If there are changes between now and November, I will provide updated analysis.

Japan’s Economy, the Yen, and the Bank of Japan

The Bank of Japan's policy of zero interest rates and ongoing asset purchases while inflation is above 2% and inflationary expectations rising is contributing to a weak yen and harming Japan's economy. Raising the BoJ's policy rate and normalizing monetary policy would boost the yen and enhance Japan's economic performance.

The Dilemmas Facing the Fed, BoE, ECB, and BoJ

Inflation has receded in the U.S., UK, EuroArea, and Japan but remains above their central banks' 2% targets. This piece assesses the different situations faced by the Fed, BoE, ECB, and BoJ, and considers the appropriate policies that would achieve their objectives and their likely course of action.